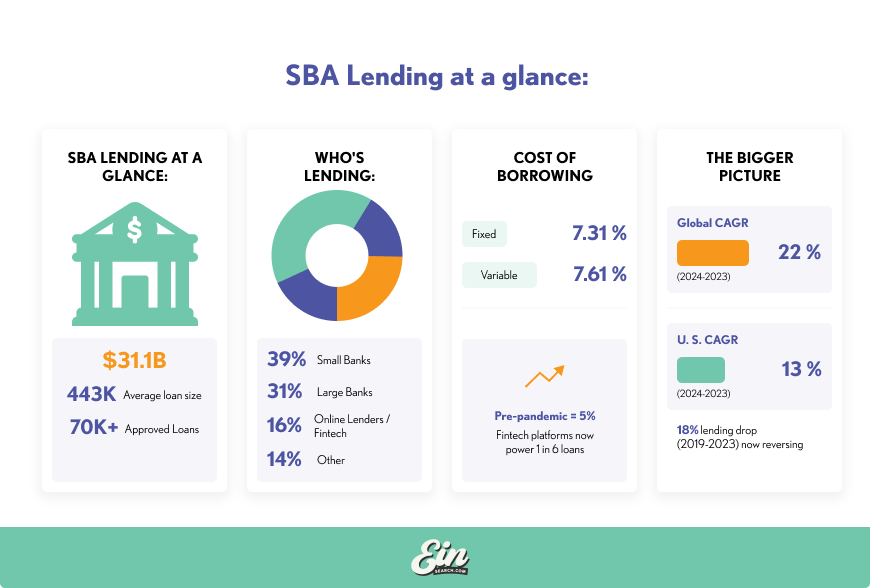

Small businesses are the backbone of the American economy, and the lending landscape that supports their growth is evolving rapidly. In 2023, the Small Business Administration (SBA) approved more than 70,000 loans worth $31.1 billion, with an average loan size of $443,000, based on data from Canopy Servicing. These figures highlight how vital access to capital remains for entrepreneurs across the United States.

The trend shows no signs of slowing. The global small business lending market is projected to grow at a compound annual growth rate (CAGR) of 22 percent from 2024, reaching approximately $7.22 trillion by 2032. Since small businesses employ nearly half of the U.S. workforce, this is not just about finance; it is about supporting the foundation of the American economy.

Here is what the latest data reveals about where small business lending stands today and how it is shaping the future of small business finance.

The Current State of Small Business Lending

After several challenging years, lending to small businesses is showing clear signs of recovery. The Kansas City Federal Reserve reports that new lending grew by 7.5% in the second quarter of 2025 compared with both the previous quarter and the same period in 2024.

Even with lending volumes increasing, banks remain cautious. Credit standards are still tight, and loan quality has shown slight deterioration, indicating that lenders are balancing optimism with careful risk management. The Kansas City Fed also found that the year-over-year growth rate in small business loan balances was 1.8%, while quarter-over-quarter growth was about 0.5%, compared to 1.0% across all loan categories.

In short, the small business lending market is expanding, but at a measured pace. Lenders are reopening access to capital gradually while maintaining a close eye on loan performance and economic stability.

Demand for Small Business Loans

On the demand side, small business borrowing activity has remained relatively stable, although the reasons for borrowing are shifting. In 2023, approximately 37% of small businesses sought some form of funding, including traditional loans, lines of credit, and merchant cash advances.

What has changed is the purpose behind the borrowing. Canopy Servicing’s data shows that most companies with annual revenues above $1 million are now seeking to expand rather than simply stay afloat. This signals growing confidence among business owners who are focusing on scaling and reinvestment.

The way businesses borrow is also evolving. Of those seeking financing, 39% applied to small banks, 31% to large banks, and 16% to online lenders. The latter figure highlights the expanding role of fintech platforms, which have made borrowing faster, more flexible, and more accessible. Digital lenders have become a key part of the financing mix for small businesses across the United States.

Approval Rates and Credit Conditions

If there is one key takeaway about credit conditions, it is that standards have tightened and continue to do so. The Kansas City Federal Reserve notes that banks have raised credit standards for 13 consecutive quarters through late 2024, marking more than three years of cautious lending.

The numbers tell the story. Small business bank lending declined by 18% nationwide between 2019 and 2023, with most regions across the country experiencing similar drops, based on figures from the St. Louis Fed. Even in the Federal Reserve’s Eighth District, lending fell by about 12% during that period.

Despite tighter lending conditions, small businesses have remained resilient. Loan application levels have stayed steady, suggesting that entrepreneurs are still seeking funding where possible. While lenders remain conservative, business owners continue to adapt through smaller loans, alternative lending sources, and SBA programs designed to fill the gaps in access to capital.

Loan Costs: Interest Rates & Terms

Borrowing costs for small businesses have increased in recent years, but context matters. Bankrate data shows the average interest rate on new small business term loans in the fourth quarter of 2024 was about 7.31% for fixed loans and 7.61% for variable loans. Just a few years earlier, pre-pandemic averages were several percentage points lower.

As of the first quarter of 2025, NerdWallet reported that small business loan rates typically range between 6.6% and 11.5%, depending on the lender and the borrower’s credit history. Meanwhile, the Kansas City Federal Reserve found that lines of credit for farmers carried a median variable rate of approximately 7.9% in urban areas and 7.4% in rural areas, with fixed options ranging from around 6.5% to 7.1%.

Lenders are also pricing risk more carefully. For term loans, the median loan spread was 255 basis points, while for lines of credit it was 313 basis points. These spreads reflect the premium borrowers pay lenders to compensate for uncertainty. For small business owners, this reinforces the importance of comparing offers, understanding terms, and ensuring that financing decisions align with long-term business goals.

Small Business Lending by Industry & Firm Size

Small businesses access capital in different ways depending on their size, industry, and stage of growth. In fiscal year 2023, the U.S. Small Business Administration supported more than 70,000 loans totaling $31.1 billion, with an average loan size of approximately $443,000, based on data compiled by Canopy Servicing. Within that, the average SBA 7(a) loan was about $480,000, with the largest reaching the program’s cap of $5 million.

For smaller enterprises and startups, the SBA Microloan Program remains a key source of financing. These loans average around $13,000 and can be as large as $50,000, offering new business owners essential working capital to build credit and fund early operations until they qualify for larger loans.

Looking ahead, technology is reshaping small business finance. The U.S. embedded and in-vehicle lending markets are projected to expand rapidly from $6.35 billion in 2024 to $23.31 billion by 2031, as digital lending becomes integrated directly into software platforms, accounting tools, and e-commerce ecosystems. This evolution promises faster, more seamless access to capital for small firms across every sector.

Challenges & Risks

Despite rising lending volumes, many small businesses still face significant barriers to financing. According to the Federal Reserve’s Small Business Credit Survey (SBCS), a substantial share of applicants continue to face difficulties obtaining the full amount of funding they seek, with approval rates varying widely by lender type.

Rising interest rates have created additional pressure. Around one-third of small firms report difficulty managing existing debt, as higher borrowing costs continue to strain cash flow.

Other ongoing challenges include:

- Rising costs and inflationary pressures

- Lengthy loan approval times

- Stricter collateral and documentation requirements

- Delinquency rates that remain above pre-pandemic levels

In short, access to credit is improving, but unevenly. While the overall lending market shows signs of recovery, many smaller firms still find themselves excluded from the opportunities needed to grow.

Outlook

The outlook for U.S. small business lending remains optimistic.

The market is projected to expand at a compound annual growth rate of approximately 13% from 2024 to 2032, representing trillions of dollars in global lending activity.

Digital transformation is a major driver of this growth. The U.S. embedded lending market is expected to increase from $6.35 billion in 2024 to $23.31 billion by 2031, while the broader digital lending sector is forecast to reach nearly $20.5 billion by 2026. As more lenders adopt digital platforms, small business owners can anticipate faster approval times, simplified applications, and more tailored loan options.

The Federal Reserve has also reported that loan originations continued to rise into early 2025, signaling steady recovery. However, challenges persist. Inflationary pressures, higher labor costs, and evolving trade policies are influencing both lending risk and pricing.

Even so, the long-term trajectory appears strong, with the market growing in size, efficiency, and technological sophistication.

Empowering Small Businesses Through Better Data

Small business lending in the United States continues to strengthen, showing steady progress across nearly every measure.

According to the latest Kansas City Fed data (as of mid-2025), new lending increased by 7.5% in Q2 2025, and the average SBA loan size reached $443,000 in fiscal year 2023. Globally, the market is expected to grow at a 22% CAGR, while in the U.S., it is projected to expand about 13% annually through 2032, underscoring its vital role in supporting business growth and economic stability.

For entrepreneurs, this means greater access to funding opportunities and a wider range of lending options. However, success still depends on being informed, prepared, and strategic in your approach to financing. Strong applications, accurate business data, and a clear understanding of the lending landscape can make all the difference.

EINsearch helps business owners and lenders alike by providing accurate, verifiable business identity data that supports transparency, compliance, and informed lending decisions. With the right insights and tools, accessing capital becomes not just possible, but predictable.